Visit the Bauxite Resources website – www.bauxiteresources.com.au

Overview of Operations

During the year the Company focused on the development of its bauxite interests in Western Australia with the objective of commercial development of bauxite and alumina capacity to support a developing market in China.

In Western Australia a number of large resource development projects have been deferred or cancelled. The aluminium industry has suffered a downturn due to lower than projected demand in China combined with a significant over supply of aluminium. Despite these concerns about the global conditions, the Company remains optimistic about the outlook for bauxite and alumina in the medium to longer term. Industry projections are that there will be increased demand from China for bauxite in the years to come. It is also expected that there will be increased political restraints on the availability of Indonesian bauxite which has been a major supplier of bauxite to China in recent years. Australian producers stand to benefit, given our geographical proximity to China.

The Company’s strategic focus from now is to:

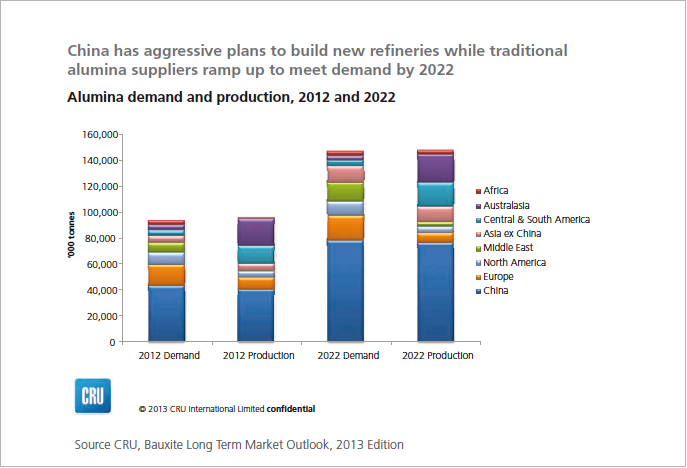

In 2013 CRU forecasts total Chinese imports to reach 60 million tonnes and 95 million tonnes by 2022. This is a substantial increase from the 38 million tonnes imported in 2012.

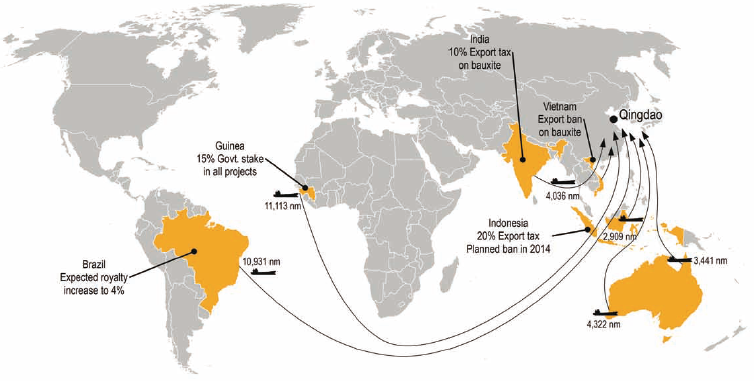

Compounding the increase in bauxite demand from China is the proposed Indonesian ban on bauxite exports, or the imposition of significant export duties. Whilst it is still expected that bauxite will continue to be exported, the general consensus is that the imposition of significant export duties by Indonesia will mean exports of bauxite will not increase from their current levels, and are likely to drop. The imposition of significant export duties on Indonesian bauxite will increase the demand for Australian bauxite.

The likely impact is that Australia and Africa will be required to supply the bulk of the increased Chinese bauxite import demand and that the price of bauxite will increase to reflect the long run marginal cost of production which is predicted by CRU to stay in the $65-70/t range in the longer term.

The Company is well placed to supply this market with a resource base presently in excess of 250 million tonnes situated close to existing rail and port infrastructure. Bauxite Resources Ltd has the largest JORC resource of all junior bauxite participants in Australia and has the potential to become one of the leading developers of bauxite in the coming years.

The Company has a beneficial interest in 97 exploration licences covering 17,710km2 (51 tenements granted covering 9,355km2) Centerd around the highly-prospective Darling Range in south west Western Australia (the largest bauxite and alumina producing region in the world). This substantial land holding is supported through exploration by BRL and also through the Company’s established joint ventures (JV) with Yankuang Resources Pty Limited (Yankuang) and HD Mining & Investment Pty Limited (HDM). The JVs allow BRL to share exploration expenditure and development costs.

BRL’s tenements in the Darling Range have significant potential to make BRL a substantial bauxite player in Australia. With global resources currently of 256.4Mt in this region this is the largest independent resource base of bauxite outside the major bauxite/alumina producers in Australia.

This current resource is of similar quality to the bauxite currently used in a number of Western Australian refineries who are some of the lowest cost producers in the world. A fundamental reason for the efficiency of Darling Range bauxite is due to its gibbsitic nature that requires low temperatures and pressure for alumina refining, thereby reducing refining costs. Another attractive element of the Company’s resources is the low level of silica, especially reactive silica (a key determinant of caustic efficiency in alumina refining).

BRL’s development strategy involves establishment of resources which are suitable for supply into the bauxite export market as well as supporting the local refining of bauxite.

In January 2011, BRL executed JV agreements with Yankuang Resources Pty Ltd for the development of both bauxite mining and alumina refining in Western Australia. To date the JV has defined 188.2 million tonnes of bauxite of which 147.9Mt is in the JV’s flagship Felicitas Deposit in the Northern Darling Range Region. The current resource at Felicitas is now at a scale to support the development of an alumina refinery in Western Australia, which is contemplated in the Alumina Refinery Joint Venture Agreement also signed in January 2011.

In 2010 the Company entered into a joint venture with HDM a wholly-owned subsidiary of the Shandong Bureau No1 Institute for Prospecting of Geology & Minerals (Shandong) to explore for bauxite. The JV allows for HDM to fund 100% of all exploration and feasibility costs for HDM to earn 60% of the bauxite rights upon a decision to mine. BRL announced the 15Mt Ceres bauxite resource in July 2012, part of the Company’s emerging Williams area and contained within the HDM joint venture in the eastern Darling Range region. The joint venture has approved further exploration drilling in the region over this years summer drilling season.

BRL retains bauxite rights to a large holding of highly prospective tenements in a world class bauxite province and has the largest independent resource base of bauxite in Australia outside the major bauxite/alumina producers.